The swipe turned dating into a habit, and Tinder still drives roughly 1.6 billion of them a day. But the headline number everyone repeats, 75 million users, hides the real story of 2026. Tinder is the biggest dating app on earth and a business in the middle of a turnaround, fighting eight straight quarters of shrinking paying subscribers while Hinge eats into its lead.

Most Tinder statistics blur two very different numbers. Monthly active users and paying subscribers are not the same, and the gap between them is enormous. This piece separates the real Tinder statistics from the inflated ones, pulls the hard figures from Match Group’s own filings, and shows where the app actually stands in 2026.

💡 Quick Tip: When a post says “Tinder has 75 million users,” that is monthly active users, not customers. Only about 8.6 million of them pay. Any article that lists a single “users” number is hiding the 9-to-1 gap between people who swipe and people who subscribe.

Tinder vs Bumble vs Hinge in 2026

Tinder no longer owns dating. Here is the three-way fight, based on Match Group filings and 2026 market data.

App | Key Edge | Best For |

Tinder | Largest user pool, ~25 to 29% US share | Volume, quick matches, casual to serious |

Hinge | Fastest growth, payers up about 15 to 17% | Serious daters wanting deeper profiles |

Bumble | Women message first | Users tired of being bombarded |

Tinder still leads on raw scale. The trouble is direction. Tinder’s payers are shrinking while Hinge, also owned by Match Group, is the one growing fast. The fight is no longer about who is biggest. It is about who is gaining.

How Many People Actually Use Tinder?

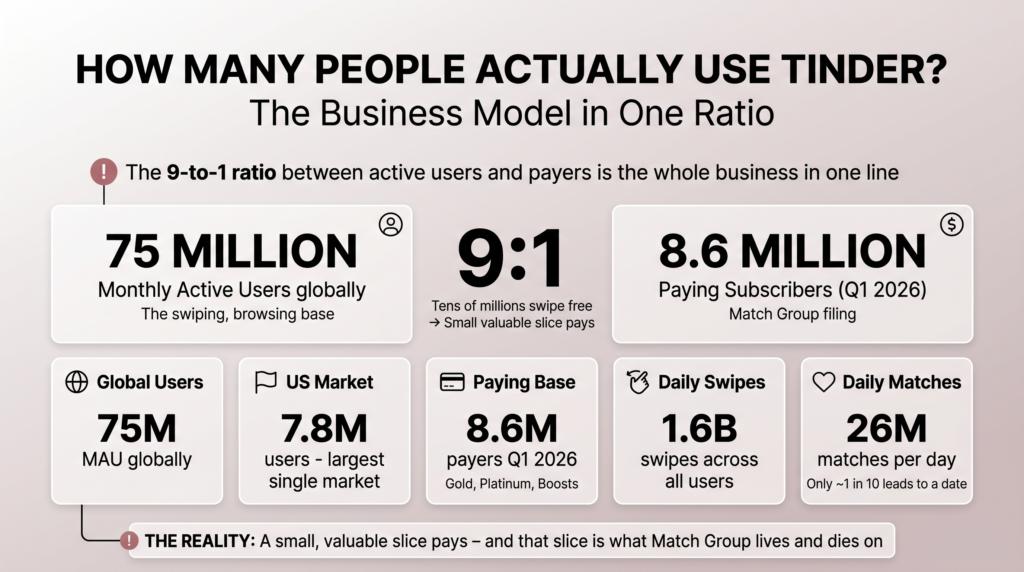

The active-user number is about 75 million monthly active users globally, with 7.8 million in the United States, per Business of Apps. That is the swiping, browsing base. The paying base is far smaller. Tinder ended Q1 2026 with about 8.6 million payers, according to Match Group’s filing.

Tinder Usage Highlights

Monthly active users: about 75 million globally

Paying subscribers: about 8.6 million as of Q1 2026

Daily swipes: roughly 1.6 billion across all users

Daily matches: around 26 million, though only about 1 in 10 leads to a date

US users: about 7.8 million, the largest single market

The 9-to-1 ratio between active users and payers is the whole business in one line. Tens of millions swipe for free. A small, valuable slice pays for Gold, Platinum, and Boosts, and that slice is what Match Group lives and dies on.

The Subscriber Story: Eight Quarters of Decline, Then a Turn

Here is the part the old user-growth charts get wrong by labeling subscribers as “total users.” Tinder’s paying base has been shrinking, not growing.

Period | Payers (millions) | Trend |

Q4 2025 | 8.77 | Down 8% year over year |

Q1 2026 | 8.6 | Down 5% year over year, an improvement |

Tinder posted negative payer growth in every quarter of 2025, eight consecutive quarters of decline across the run. The small bright spot is that Q1 2026 slowed the bleed, a 5% drop versus 8% the quarter before. Match Group is calling this early momentum, crediting better product experiences for Gen Z, and has set a goal to re-establish Tinder as a growth business in 2027. The company is not there yet. The trend is less bad, not yet good.

How Tinder Makes Money

Tinder is free to download and runs a freemium model that funnels users toward subscriptions and à la carte buys. Even with fewer payers, it remains the biggest revenue engine in Match Group’s portfolio.

How Tinder Earns

Tinder Plus: entry tier with unlimited swipes, Rewind, and Passport

Tinder Gold: adds Likes You, so you see who already swiped right

Tinder Platinum: top tier with Priority Likes and Message Before Matching

À la carte: Super Likes and Boosts bought individually

Revenue per payer: about $17.56 a month in Q1 2026, up 7% year over year

The money math for 2025 tells the turnaround story. Tinder generated about $1.9 billion in direct revenue for the full year, down 4% from the year before. It is still by far the largest contributor to Match Group’s roughly $3.5 billion in total 2025 revenue. The clever part is that Tinder is squeezing more from each remaining payer. Fewer subscribers, but each one pays more, which is how revenue has held up better than the subscriber count alone would suggest.

Who Uses Tinder?

The audience is young and heavily male, and that imbalance shapes everything about the experience.

Tinder Audience Highlights

Age: about 61% of users are 18 to 34, with the 18-24 group the largest

Gender: roughly 75.8% male and 24.2% female

Top market: the United States, with about 7.8 million users and 40% of revenue

Global reach: available in more than 190 countries

Other big markets: the UK, Brazil, Canada, France, Australia, and Germany

The gender split is the most talked-about Tinder statistic, and for good reason. At nearly three men for every woman, the experience splits hard by gender. Men face heavy competition and fewer matches. Women get flooded with likes. The ratio is wider still in markets like India and closer to even in parts of Europe.

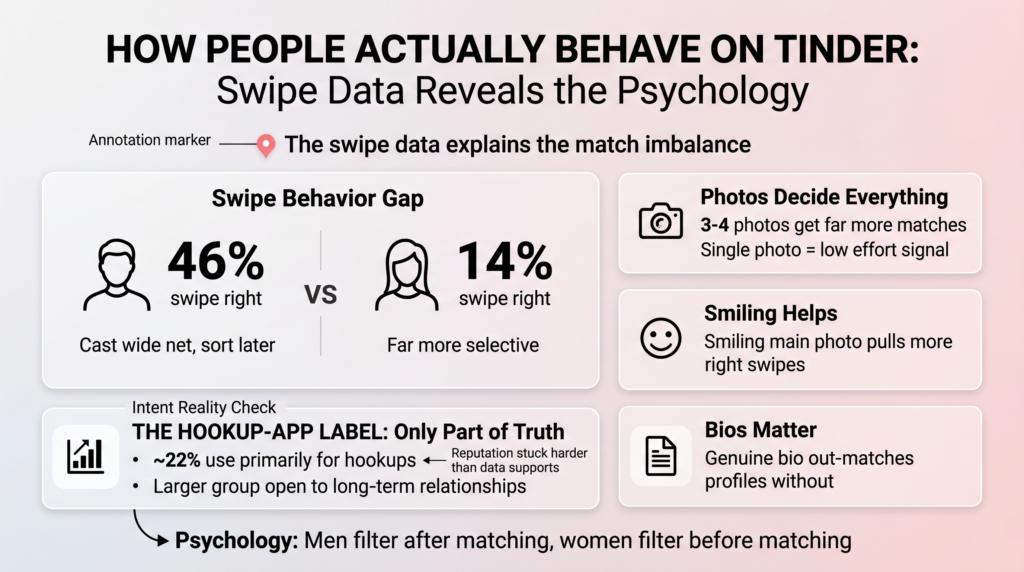

How People Actually Behave on Tinder

The swipe data reveals the psychology behind the app, and it explains the match imbalance.

Men swipe right on about 46% of profiles. They cast a wide net and sort later.

Women swipe right on about 14% of profiles. They are far more selective.

Photos decide everything. Profiles with 3 to 4 photos get far more matches than single-photo profiles, which often read as low effort.

Smiling helps. A smiling main photo pulls more right swipes.

Bios matter. A profile with a genuine bio out-matches one without.

On intent, the hookup-app label is only part of the truth. Surveys put the share who use Tinder primarily for hookups at around 22%, while a larger group is open to a long-term relationship. The reputation stuck harder than the data supports.

Tinder vs the Competition: The Real Fight

Tinder still holds the most US market share, roughly 25 to 29%, with Bumble close behind around 24 to 26% and Hinge near 18%. The momentum numbers are what matter. While Tinder’s payers fell 8% in Q4 2025, Hinge’s payers grew about 15 to 17% and its revenue surged in the mid-20s percent range. Bumble has struggled harder than both, with revenue down about 10% and paying users down 16% in recent quarters.

The takeaway is uncomfortable for Tinder. Its own corporate sibling, Hinge, is the growth story, marketed as the app designed to be deleted and winning the serious-dater crowd with deeper profiles and AI-driven features. Tinder has the largest pool, but Hinge earns more per user and is climbing while Tinder fights to stabilize.

Tinder Pros and Cons

Pros

The largest user base in dating, about 75 million MAU

Still the biggest revenue engine in Match Group, about $1.9 billion in 2025

Rising revenue per payer, up 7% to about $17.56, offsetting subscriber loss

Cons

Eight straight quarters of payer decline before Q1 2026 eased it

A heavy gender imbalance, roughly 76% male, that hurts the experience for men

Losing momentum to Hinge, which is growing payers and revenue while Tinder shrinks

🎯 Why Tinder still matters: No dating app comes close on scale. With about 75 million monthly active users, 1.6 billion daily swipes, and $1.9 billion in revenue, Tinder is still the giant of the category. The 2026 story is whether it can turn shrinking subscribers into the growth Match Group is promising for 2027.

FAQs

Tinder has approximately 75 million monthly active users worldwide in 2026, including around 7.8 million in the United States. Of those global users, roughly 8.6 million pay for a subscription as of Q1 2026.

Yes, Tinder leads US market share at roughly 25 to 29%, ahead of Bumble at 24 to 26% and Hinge at around 18%. However, Hinge is the fastest-growing competitor, with paying subscribers rising 15 to 17% while Tinder's continue to decline.

Tinder's user base skews heavily male, at approximately 75.8% men versus 24.2% women globally. The gap is especially wide in markets like India, which creates more competition among male users and higher match rates for female users.

Tinder operates on a freemium model, offering paid subscription tiers — Plus, Gold, and Platinum — alongside à la carte purchases like Super Likes and Boosts. A small percentage of users pay, but they generate enough revenue to support the entire platform, with average monthly revenue per payer reaching about $17.56.

Match Group believes so, pointing to a slowdown in the rate of decline to around 5% year over year in Q1 2026 as early evidence of a potential turnaround. The company has framed this deceleration as momentum toward stabilizing and growing its paying subscriber base by 2027, though the streak of eight consecutive quarterly declines makes recovery uncertain.